Time series cross-validation evaluates a model’s predictive performance by training on past data and testing on subsequent time periods using a sliding window approach.

MLForecast offers an efficient and easy-to-use implementation of this technique.

To see how to implement time series cross-validation with MLForecast, let’s start reading a subset of the M4 Competition hourly dataset.

import pandas as pd

from utilsforecast.plotting import plot_series

Y_df = pd.read_csv("https://datasets-nixtla.s3.amazonaws.com/m4-hourly.csv").query(

"unique_id == 'H1'"

)

Y_df unique_id ds y

0 H1 1 605.0

1 H1 2 586.0

2 H1 3 586.0

3 H1 4 559.0

4 H1 5 511.0

.. ... ... ...

743 H1 744 785.0

744 H1 745 756.0

745 H1 746 719.0

746 H1 747 703.0

747 H1 748 659.0

[748 rows x 3 columns]Plot the time series:

fig = plot_series(Y_df, plot_random=False, max_insample_length=24 * 14)

fig

Instantiate a new MLForecast object:

from mlforecast import MLForecast

from mlforecast.target_transforms import Differences

from sklearn.linear_model import LinearRegression

mlf = MLForecast(

models=[LinearRegression()],

freq=1,

target_transforms=[Differences([24])],

lags=range(1, 25),

)Once the MLForecast object has been instantiated, we can use the cross_validation method.

For this particular example, we’ll use 3 windows of 24 hours.

# use 3 windows of 24 hours

cross_validation_df = mlf.cross_validation(

df=Y_df,

h=24,

n_windows=3,

)

cross_validation_df.head() unique_id ds cutoff y LinearRegression

0 H1 677 676 691.0 676.726797

1 H1 678 676 618.0 559.559522

2 H1 679 676 563.0 549.167938

3 H1 680 676 529.0 505.930997

4 H1 681 676 504.0 481.981893

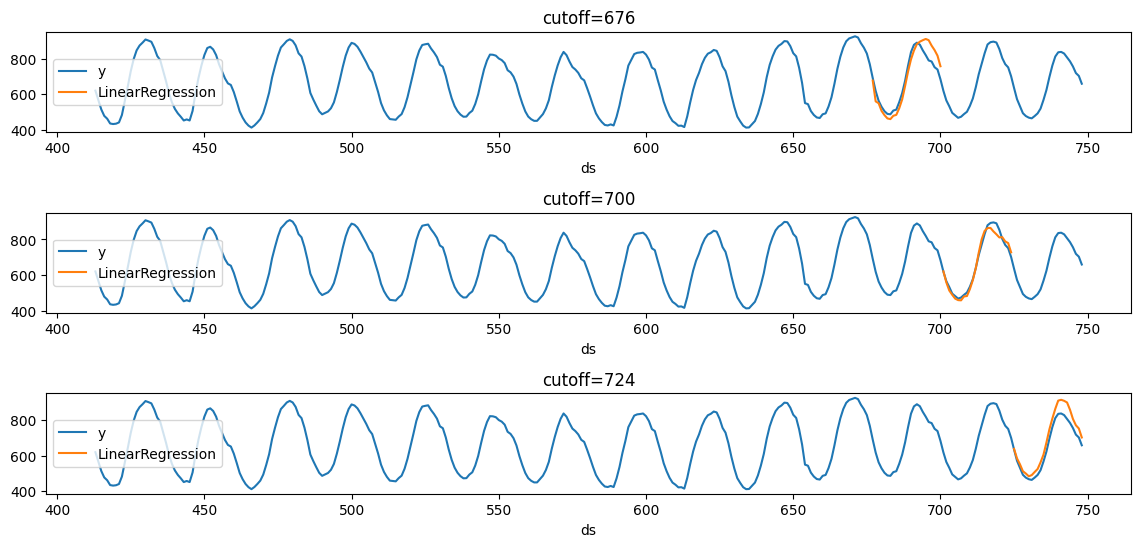

We’ll now plot the forecast for each cutoff period.

import matplotlib.pyplot as plt

def plot_cv(df, df_cv, last_n=24 * 14):

cutoffs = df_cv["cutoff"].unique()

fig, ax = plt.subplots(

nrows=len(cutoffs), ncols=1, figsize=(14, 6), gridspec_kw=dict(hspace=0.8)

)

for cutoff, axi in zip(cutoffs, ax.flat):

df.tail(last_n).set_index("ds").plot(ax=axi, y="y")

df_cv.query("cutoff == @cutoff").set_index("ds").plot(

ax=axi,

y="LinearRegression",

title=f"{cutoff=}",

)

plot_cv(Y_df, cross_validation_df)

Notice that in each cutoff period, we generated a forecast for the next 24 hours using only the data y before said period.