PySpark is a powerful tool for big data processing, but it lacks native support for time series data.

Tempo fills this gap with a more intuitive API, making it easier to perform common tasks like resampling and aggregating time-series data.

In this blog post, we’ll explore some examples that compare PySpark and Tempo, highlighting the benefits of using Tempo for time-series data analysis.

Data Preparation

Before we dive into the examples, let’s prepare our data. We’ll create a sample dataset of market data with the following columns:

symbol: the stock symbol (e.g. “AAPL” or “GOOGL”)event_ts: the timestamp of the event (e.g. “2024-01-01 09:30:00”)price: the current price of the stockvolume: the number of shares tradedbid: the current bid priceask: the current ask price

Here’s the code to create the sample dataset:

from pyspark.sql import functions as F

from pyspark.sql import Window

# Create sample market data

market_data = [

("AAPL", "2024-01-01 09:30:00", 180.50, 1000, 180.45, 180.55),

("AAPL", "2024-01-01 09:30:05", 180.52, 1200, 180.48, 180.58),

("AAPL", "2024-01-01 09:30:10", 180.48, 800, 180.45, 180.52),

("AAPL", "2024-01-01 09:30:15", 180.55, 1500, 180.50, 180.60),

("GOOGL", "2024-01-01 09:30:00", 140.25, 500, 140.20, 140.30),

("GOOGL", "2024-01-01 09:30:05", 140.30, 600, 140.25, 140.35),

("GOOGL", "2024-01-01 09:30:10", 140.28, 450, 140.25, 140.32),

("GOOGL", "2024-01-01 09:30:15", 140.32, 700, 140.28, 140.38),

]

# Create DataFrame

market_df = spark.createDataFrame(

market_data, ["symbol", "event_ts", "price", "volume", "bid", "ask"]

)

# Convert timestamp string to timestamp type

market_df = market_df.withColumn("event_ts", F.to_timestamp("event_ts"))Next, we’ll create a Tempo TSDF (Time Series DataFrame) from the market_df DataFrame. We’ll specify the event_ts column as the timestamp column and the partition column.

from tempo import *

# Create Tempo TSDF

market_tsdf = TSDF(market_df, ts_col="event_ts", partition_cols=["symbol"])Now we’re ready to explore the examples!

Example 1: Get Data at Specific Time

Suppose we want to get the data at a specific time, say 2024-01-01 09:30:10. With PySpark, we would use the filter method to achieve this:

target_time = "2024-01-01 09:30:10"

pyspark_at_target = market_df.filter(F.col("event_ts") == target_time)

pyspark_at_target.show()With Tempo, we can use the at method to achieve the same result:

tempo_at_target = market_tsdf.at(target_time)

tempo_at_target.show()Both methods produce the same output:

+------+-------------------+------+------+------+------+

|symbol| event_ts| price|volume| bid| ask|

+------+-------------------+------+------+------+------+

| AAPL|2024-01-01 09:30:10|180.48| 800|180.45|180.52|

| GOOGL|2024-01-01 09:30:10|140.28| 450|140.25|140.32|

+------+-------------------+------+------+------+------+Example 2: Get Data between Time Interval

Suppose we want to get the data between a time interval, say 2024-01-01 09:30:05 and 2024-01-01 09:30:15. With PySpark, we would use the filter method with a conditional statement:

start_ts = "2024-01-01 09:30:05"

end_ts = "2024-01-01 09:30:15"

pyspark_interval = market_df.filter(

(F.col("event_ts") >= start_ts) & (F.col("event_ts") <= end_ts)

)

pyspark_interval.show()With Tempo, we can use the between method to achieve the same result:

tempo_interval = market_tsdf.between(start_ts, end_ts)

tempo_interval.show()Both methods produce the same output:

+------+-------------------+------+------+------+------+

|symbol| event_ts| price|volume| bid| ask|

+------+-------------------+------+------+------+------+

| AAPL|2024-01-01 09:30:05|180.52| 1200|180.48|180.58|

| AAPL|2024-01-01 09:30:10|180.48| 800|180.45|180.52|

| AAPL|2024-01-01 09:30:15|180.55| 1500| 180.5| 180.6|

| GOOGL|2024-01-01 09:30:05| 140.3| 600|140.25|140.35|

| GOOGL|2024-01-01 09:30:10|140.28| 450|140.25|140.32|

| GOOGL|2024-01-01 09:30:15|140.32| 700|140.28|140.38|

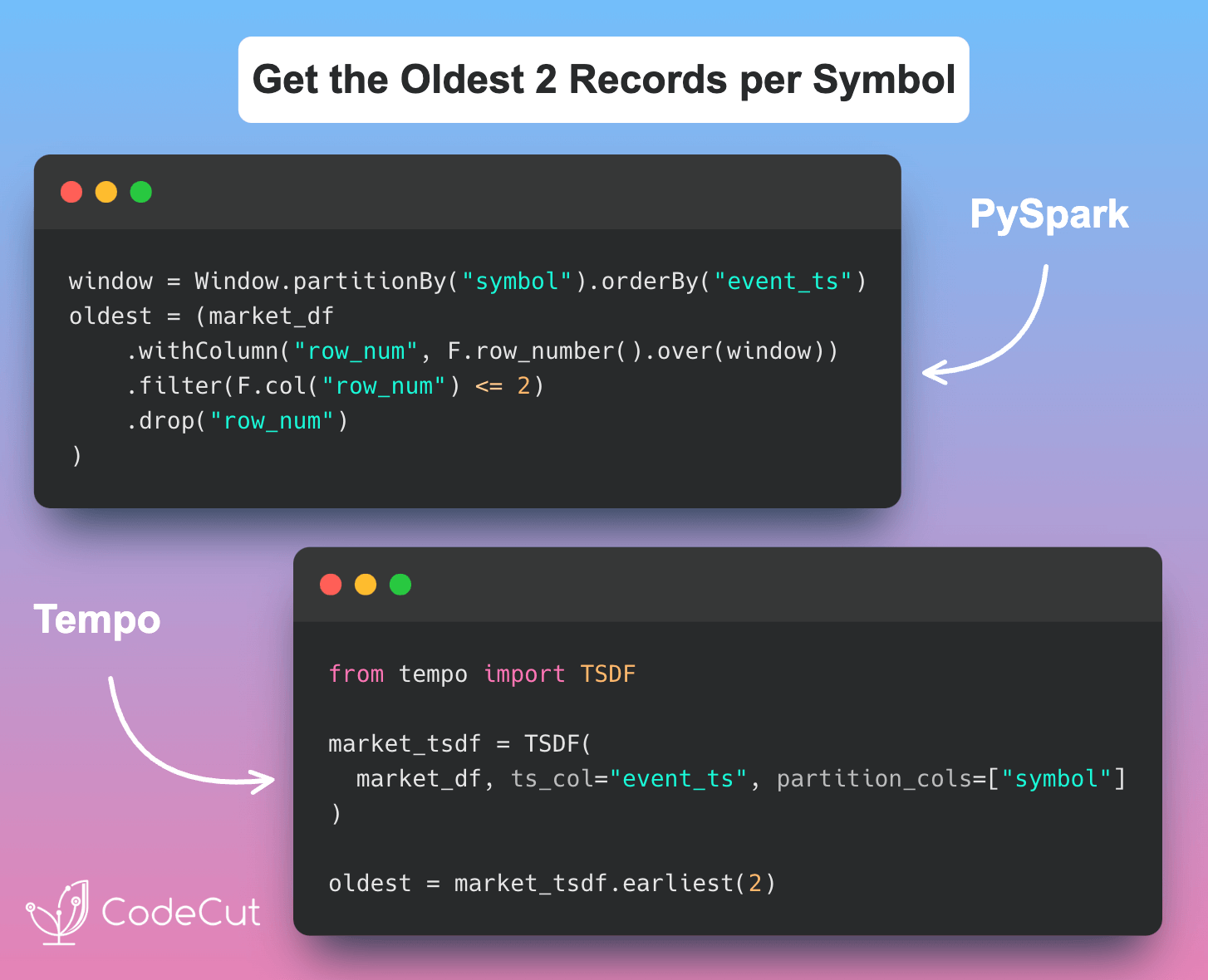

+------+-------------------+------+------+------+------+Example 3: Get the Oldest N Records per Symbol

Suppose we want to get the oldest N records per symbol, say N=2. With PySpark, we would use the row_number function with a window specification:

n = 2

windowSpec = Window.partitionBy("symbol").orderBy("event_ts")

pyspark_oldest = (

market_df.withColumn("row_num", F.row_number().over(windowSpec))

.filter(F.col("row_num") <= n)

.drop("row_num")

)

pyspark_oldest.show()With Tempo, we can use the earliest method to achieve the same result:

tempo_oldest = market_tsdf.earliest(n)

tempo_oldest.show()Both methods produce the same output:

+------+-------------------+------+------+------+------+

|symbol| event_ts| price|volume| bid| ask|

+------+-------------------+------+------+------+------+

| AAPL|2024-01-01 09:30:00| 180.5| 1000|180.45|180.55|

| AAPL|2024-01-01 09:30:05|180.52| 1200|180.48|180.58|

| GOOGL|2024-01-01 09:30:00|140.25| 500| 140.2| 140.3|

| GOOGL|2024-01-01 09:30:05| 140.3| 600|140.25|140.35|

+------+-------------------+------+------+------+------+Example 4: Moving Averages

Suppose we want to calculate the moving average of the price column with a 10-second window. With PySpark, we would use the avg function with a window specification:

market_df = market_df.withColumn("event_ts_seconds", F.unix_timestamp("event_ts"))

movingWindowSpec = (

Window.partitionBy("symbol").orderBy("event_ts_seconds").rangeBetween(-10, 0)

)

pyspark_moving_stats = market_df.withColumn(

"mean_price", F.avg("price").over(movingWindowSpec)

)

pyspark_moving_stats.select("symbol", "event_ts", "price", "mean_price").show()With Tempo, we can use the withRangeStats method to achieve the same result:

tempo_moving_stats = market_tsdf.withRangeStats("price", rangeBackWindowSecs=10)

tempo_moving_stats.select("symbol", "event_ts", "price", "mean_price").show()Both methods produce the same output:

+------+-------------------+------+------------------+

|symbol| event_ts| price| mean_price|

+------+-------------------+------+------------------+

| AAPL|2024-01-01 09:30:00| 180.5| 180.5|

| AAPL|2024-01-01 09:30:05|180.52| 180.51|

| AAPL|2024-01-01 09:30:10|180.48| 180.5|

| AAPL|2024-01-01 09:30:15|180.55|180.51666666666665|

| GOOGL|2024-01-01 09:30:00|140.25| 140.25|

| GOOGL|2024-01-01 09:30:05| 140.3| 140.275|

| GOOGL|2024-01-01 09:30:10|140.28|140.27666666666667|

| GOOGL|2024-01-01 09:30:15|140.32| 140.3|

+------+-------------------+------+------------------+Example 5: Grouped Statistics

Suppose we want to calculate the mean, min, and max of the price column grouped by symbol and a 5-second window. With PySpark, we would use the groupBy method with a window specification:

pyspark_grouped = market_df.groupBy("symbol", F.window("event_ts", "5 seconds")).agg(

F.avg("price").alias("mean_price"),

F.min("price").alias("min_price"),

F.max("price").alias("max_price"),

)

pyspark_grouped.show()Output:

+------+--------------------+----------+---------+---------+

|symbol| window|mean_price|min_price|max_price|

+------+--------------------+----------+---------+---------+

| AAPL|{2024-01-01 09:30...| 180.5| 180.5| 180.5|

| AAPL|{2024-01-01 09:30...| 180.52| 180.52| 180.52|

| AAPL|{2024-01-01 09:30...| 180.48| 180.48| 180.48|

| AAPL|{2024-01-01 09:30...| 180.55| 180.55| 180.55|

| GOOGL|{2024-01-01 09:30...| 140.25| 140.25| 140.25|

| GOOGL|{2024-01-01 09:30...| 140.3| 140.3| 140.3|

| GOOGL|{2024-01-01 09:30...| 140.28| 140.28| 140.28|

| GOOGL|{2024-01-01 09:30...| 140.32| 140.32| 140.32|

+------+--------------------+----------+---------+---------+With Tempo, we can use the withGroupedStats method to achieve the same result:

tempo_grouped = market_tsdf.withGroupedStats(

metricCols=["price"], freq="5 seconds"

)

tempo_grouped.show()Output:

+------+-------------------+----------+---------+---------+

|symbol| event_ts|mean_price|min_price|max_price|

+------+-------------------+----------+---------+---------+

| AAPL|2024-01-01 09:30:00| 180.5| 180.5| 180.5|

| AAPL|2024-01-01 09:30:05| 180.52| 180.52| 180.52|

| AAPL|2024-01-01 09:30:10| 180.48| 180.48| 180.48|

| AAPL|2024-01-01 09:30:15| 180.55| 180.55| 180.55|

| GOOGL|2024-01-01 09:30:00| 140.25| 140.25| 140.25|

| GOOGL|2024-01-01 09:30:05| 140.3| 140.3| 140.3|

| GOOGL|2024-01-01 09:30:10| 140.28| 140.28| 140.28|

| GOOGL|2024-01-01 09:30:15| 140.32| 140.32| 140.32|

+------+-------------------+----------+---------+---------+Tempo provides a more intuitive and concise API for working with time-series data, making it easier to perform common tasks like resampling and aggregating time-series data.